ECONOMIC SURVEY 2022-23

The Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman tabled the Economic Survey 2022-23 in Parliament on 31 January 2023, which projects a baseline GDP growth of 6.5 per cent in real terms in FY24. The projection is broadly comparable to the estimates provided by multilateral agencies such as the World Bank, the IMF, and the ADB and by RBI, domestically. It says, growth is expected to be brisk in FY24 as a vigorous credit disbursal, and capital investment cycle is expected to unfold in India with the strengthening of the balance sheets of the corporate and banking sectors. Further support to economic growth will come from the expansion of public digital platforms and path-breaking measures such as PM GatiShakti, the National Logistics Policy, and the Production-Linked Incentive schemes to boost manufacturing output. The highlights of the Survey are as follows :

State of the Economy 2022-23: Recovery Complete

• Recovering from pandemic-induced contraction, Russian-Ukraine conflict and inflation, Indian economy is staging a broad based recovery across sectors, positioning to ascend to the pre-pandemic growth path in FY23.

• India’s GDP growth is expected to remain robust in FY24. GDP forecast for FY24 to be in the range of 6-6.8 %.

• Private consumption in H1 is highest since FY15 and this has led to a boost to production activity resulting in enhanced capacity utilisation across sectors.

India’s Medium Term Growth Outlook: with Optimism and Hope

• Indian economy underwent wide-ranging structural and governance reforms that strengthened the economy’s fundamentals by enhancing its overall efficiency during 2014-2022.

• With an underlying emphasis on improving the ease of living and doing business, the reforms after 2014 were based on the broad principles of creating public goods, adopting trust-based governance, co-partnering with the private sector for development, and improving agricultural productivity.

• The period of 2014-2022 also witnessed balance sheet stress caused by the credit boom in the previous years and one-off global shocks, that adversely impacted the key macroeconomic variables such as credit growth, capital formation, and hence economic growth during this period.

• This situation is analogous to the period 1998-2002 when transformative reforms undertaken by the government had lagged growth returns due to temporary shocks in the economy. Once these shocks faded, the structural reforms paid growth dividends from 2003.

Fiscal Developments: Revenue Relish

• The Union Government finances have shown a resilient performance during the year FY23, facilitated by the recovery in economic activity, buoyancy in revenues from direct taxes and GST, and realistic assumptions in the Budget.

• The Gross Tax Revenue registered a YoY growth of 15.5 per cent from April to November 2022, driven by robust growth in the direct taxes and Goods and Services Tax (GST).

• Growth in direct taxes during the first eight months of the year was much higher than their corresponding longer-term averages.

• GST has stabilised as a vital revenue source for central and state governments, with the gross GST collections increasing at 24.8 per cent on YoY basis from April to December 2022.

• Union Government’s emphasis on capital expenditure (Capex) has continued despite higher revenue expenditure requirements during the year. The Centre’s Capex has steadily increased from a long-term average of 1.7 per cent of GDP (FY09 to FY20) to 2.5 per cent of GDP in FY22 PA.

Monetary Management and Financial Intermediation: A Good Year

• The RBI initiated its monetary tightening cycle in April 2022 and has since raised the repo rate by 225 bps, leading to moderation of surplus liquidity conditions.

• Cleaner balance sheets led to enhanced lending by financial institutions.

• The growth in credit offtake is expected to sustain, and combined with a pick-up in private capex, will usher in a virtuous investment cycle.

• Non-food credit offtake by scheduled Commercial Banks (SCBs) has been growing in double digits since April 2022.

• Credit disbursed by Non-Banking Financial Companies (NBFCs) has also been on the rise.

• The Gross Non-Performing Assets (GNPA) ratio of SCBs has fallen to a seven-year low of 5.0.

• The Capital-to-Risk Weighted Assets Ratio (CRAR) remains healthy at 16.0.

• The recovery rate for the SCBs through Insolvency and Bankruptcy (IBC) was highest in FY22 compared to other channels.

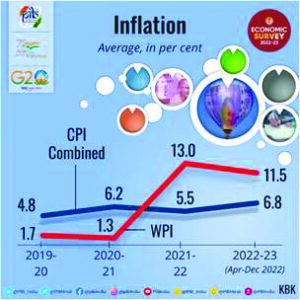

Prices and Inflation: Successful Tight-Rope Walking

• While the year 2022 witnessed a return of high inflation in the advanced world after three to four decades, India caps the rise in prices.

• While India’s retail inflation rate peaked at 7.8 per cent in April 2022, above the RBI’s upper tolerance limit of 6 per cent, the overshoot of inflation above the upper end of the target range in India was however one of the lowest in the world.

• The government adopted a multi-pronged approach to tame the increase in price levels

o Phase wise reduction in export duty of petrol and diesel

o Import duty on major inputs were brought to zero while tax on export of iron ores and concentrates increased from 30 to 50 per cent

o Waived customs duty on cotton imports w.e.f 14 April 2022, until 30 September 2022

o Prohibition on the export of wheat products under HS Code 1101 and imposition of export duty on rice

o Reduction in basic duty on crude and refined palm oil, crude soyabean oil and crude sunflower oil

• The RBI’s anchoring of inflationary expectations through forward guidance and responsive monetary policy has helped guide the trajectory of inflation in the country.

• The one-year-ahead inflationary expectations by both businesses and households have moderated in the current financial year.

• Timely policy intervention by the government in housing sector, coupled with low home loan interest rates propped up demand and attracted buyers more readily in the affordable segment in FY23.

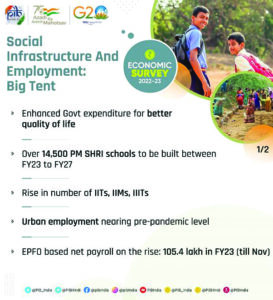

Social Infrastructure and Employment : Big Tent

• Social Sector witnessed significant increase in government spending.

• Central and State Government’s budgeted expenditure on health sector touched 2.1% of GDP in FY23 (BE) and 2.2% in FY22 (RE) against 1.6% in FY21.

• Social sector expenditure increases to Rs. 21.3 lakh crore in FY23 (BE) from Rs. 9.1 lakh crore in FY16.

• Survey highlights the findings of the 2022 report of the UNDP on Multidimensional Poverty Index which says that 41.5 crore people exit poverty in India between 2005-06 and 2019-20.

• The Aspirational Districts Programme has emerged as a template for good governance, especially in remote and difficult areas.

• eShram portal developed for creating a National database of unorganised workers, which is verified with Aadhaar. As on 31 December 2022, a total of over 28.5 crore unorganised workers have been registered on eShram portal.

• JAM (Jan-Dhan, Aadhaar, and Mobile) trinity, combined with the power of DBT, has brought the marginalised sections of society into the formal financial system, revolutionising the path of transparent and accountable governance by empowering the people.

• Aadhaar played a vital role in developing the Co-WIN platform and in the transparent administration of over 2 billion vaccine doses.

• Labour markets have recovered beyond pre-Covid levels, in both urban and rural areas, with unemployment rates falling from 5.8 per cent in 2018-19 to 4.2 per cent in 2020-21.

Climate Change and Environment: Preparing to Face the Future

• India declared the Net Zero Pledge to achieve net zero emissions goal by 2070.

• India achieved its target of 40 per cent installed electric capacity from non-fossil fuels ahead of 2030.

• The likely installed capacity from non-fossil fuels to be more than 500 GW by 2030 resulting in decline of average emission rate by around 29% by 2029-30, compared to 2014-15.

• India to reduce emissions intensity of its GDP by 45% by 2030 from 2005 levels.

• About 50% cumulative electric power installed capacity to come from non-fossil fuel-based energy resources by 2030.

• A mass movement LIFE– Life style for Environment launched.

• Sovereign Green Bond Framework (SGrBs) issued in November 2022.

• RBI auctions two tranches of Rs. 4,000 crore Sovereign Green Bonds (SGrB).

• National Green Hydrogen Mission to enable India to be energy independent by 2047.

Agriculture and Food Management

• The performance of the agriculture and allied sector has been buoyant over the past several years, much of which is on account of the measures taken by the government to augment crop and livestock productivity, ensure certainty of returns to the farmers through price support, promote crop diversification, improve market infrastructure through the impetus provided for the setting up of farmer-producer organisations and promotion of investment in infrastructure facilities through the Agriculture Infrastructure Fund.

• Private investment in agriculture increases to 9.3% in 2020-21.

• MSP for all mandated crops fixed at 1.5 times of all India weighted average cost of production since 2018.

• Institutional Credit to the Agricultural Sector continued to grow to 18.6 lakh crore in 2021-22

• Foodgrains production in India saw sustained increase and stood at 315.7 million tonnes in 2021-22.

• Free foodgrains to about 81.4 crore beneficiaries under the National Food Security Act for one year from January 1, 2023.

• About 11.3 crore farmers were covered under the Scheme in its April-July 2022-23 payment cycle.

Industry: Steady Recovery

• Overall Gross Value Added (GVA) by the Industrial Sector (for the first half of FY 22-23) rose 3.7 per cent, which is higher than the average growth of 2.8 per cent achieved in the first half of the last decade.

• Robust growth in Private Final Consumption Expenditure, export stimulus during the first half of the year, increase in investment demand triggered by enhanced public capex and strengthened bank and corporate balance sheets have provided a demand stimulus to industrial growth.

• The supply response of the industry to the demand stimulus has been robust.

• PMI manufacturing has remained in the expansion zone for 18 months since July 2021, and Index of Industrial Production (IIP) grows at a healthy pace.

• Credit to Micro, Small and Medium Enterprises (MSMEs) has grown by an average of around 30% since January 2022 and credit to large industry has been showing

double-digit growth since October 2022.

• Electronics exports rise nearly threefold, from US $4.4 billion in FY19 to US $11.6 Billion in FY22.

• Igeneration of 3.0 lakh have been recorded due to PLI schemes.

• Over 39,000 compliances have been reduced and more than 3500 provisions decriminalized as of January 2023.

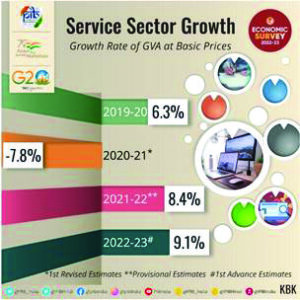

Services: Source of Strength

• The services sector is expected to grow at 9.1% in FY23, as against 8.4% (YoY) in FY22.

• Robust expansion in PMI services, indicative of service sector activity, observed since July 2022.

• India was among the top ten services exporting countries in 2021, with its share in world commercial services exports increasing from 3 per cent in 2015 to 4 per cent in 2021.

• India’s services exports remained resilient during the Covid-19 pandemic and amid geopolitical uncertainties driven by higher demand for digital support, cloud services, and infrastructure modernization.

• Credit to services sector has grown by over 16% since July 2022.

• US$ 7.1 billion FDI equity inflows in services sector in FY22.